Whether you’re 25 or 40, it’s natural to wonder: “Am I saving enough?” It’s a question packed with emotion—and often without a clear answer. While everyone’s financial path is different, looking at average American savings by age can offer a helpful benchmark. And if you’re asking “how much money should I have saved by 30?” or “how far behind am I at 40?”, you’re definitely not alone.

This article breaks down national savings data and includes realistic benchmarks for where your savings might stand—and where you can still go from here.

What Counts as “Savings”?

For clarity, this article looks at total liquid and retirement savings, including:

Cash in savings or checking accounts

401(k), IRA, and other retirement accounts

Brokerage accounts (taxable investments)

We don’t include home equity or illiquid assets—this is about what’s ready for emergencies, growth, or retirement.

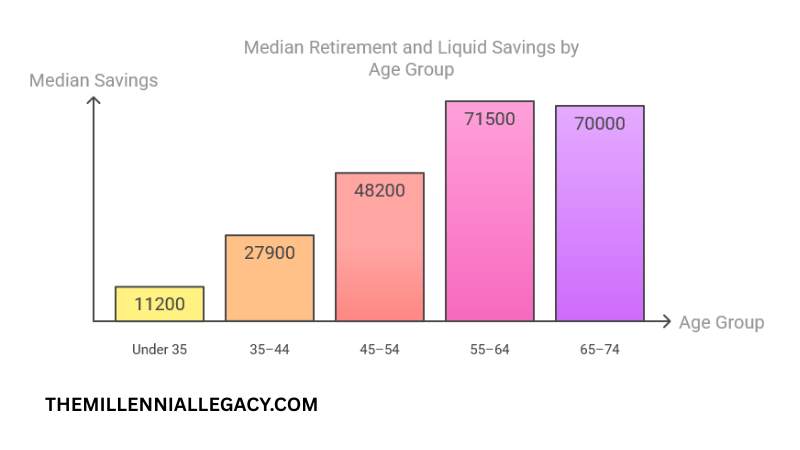

Average American Savings by Age

According to the Federal Reserve’s 2022 Survey of Consumer Finances, here’s how the median savings (including retirement accounts) stack up by age group:

These figures offer a reality check. They reflect what people have—not what financial experts recommend.

Under 35 ($11,200): This is typically a stage where income is still ramping up and financial obligations like rent, debt repayment, or education costs can take priority over saving. Many in this age range are just starting to build their financial foundation.

35–44 ($27,900): At this stage, earnings are typically higher—but so are expenses, including housing, family costs, and possibly aging parent support. Savings may be growing, but slowly.

45–54 ($48,200): With retirement starting to appear on the horizon, this age group ideally should have already built a solid savings base. But in practice, many are still catching up or restarting after financial setbacks.

55–64 ($71,500): This is often considered the final decade before retirement, yet the median amount saved remains far below most retirement income recommendations. It raises concern about long-term security for a large portion of households.

65–74 ($70,000): For those already retired or just entering retirement, this figure reflects both savings that remain and the financial limitations many face. It suggests a reliance on fixed income sources like Social Security rather than personal assets.

A Note on “Median” vs. “Average”

You might have seen headlines stating that the average 401(k) balance is well over $100,000—and technically, that’s true. But average figures are skewed by a small number of very high-balance accounts. The median, on the other hand, gives a clearer view of what most people have saved.

So when the median savings for a 55–64-year-old is reported as $71,500, that means half of people in that group have saved less than that amount—a far more realistic snapshot of typical households in America.

Average Savings by Age 25

If you’re wondering about the average savings by age 25, here’s what the data says:

The average 25-year-old has $3,240 in savings, according to SmartAsset.

Many have $0 saved for retirement—especially if they’re still paying off student loans.

For someone making $40,000/year, that’s $20,000–$40,000—a stretch for most 25-year-olds, but a useful long-term benchmark.

How Much Money Should I Have Saved by 30?

This question gets Googled thousands of times every month. According to Fidelity’s age-based savings guidelines, by age 30, you should aim to have 1x your annual salary saved for retirement.

So if you earn $50,000/year, your goal would be $50,000 in total savings (retirement + other).

But how are people actually doing?

The average savings for 30-somethings is around $11,200, according to Federal Reserve data.

Bottom line: If you’re behind, you’re in good company—but catching up is still possible.

Average Savings by Age 40

By age 40, many people are balancing kids, mortgages, career shifts, and often feel squeezed between saving and spending.

The average savings by age 40 is about $27,900, per the Federal Reserve

Fidelity recommends having 3x your salary saved by 40

So, if you earn $75,000/year, the goal would be $225,000 in retirement and savings

How much money should I have saved by 40? It depends on your lifestyle, debt, and goals—but aiming for at least 2–3x your annual income is a common benchmark.

Why So Many Are Behind (And What to Do About It)

Across all age groups, savings rates are lower than ideal. Here’s why:

Student debt delayed saving for Millennials

Stagnant wages have made it harder to grow wealth

Housing costs have outpaced income growth in most major cities

Low financial literacy remains a persistent challenge

But here’s the good news: starting now still matters. Even if you’re in your 40s or 50s, there’s time to catch up—especially if you:

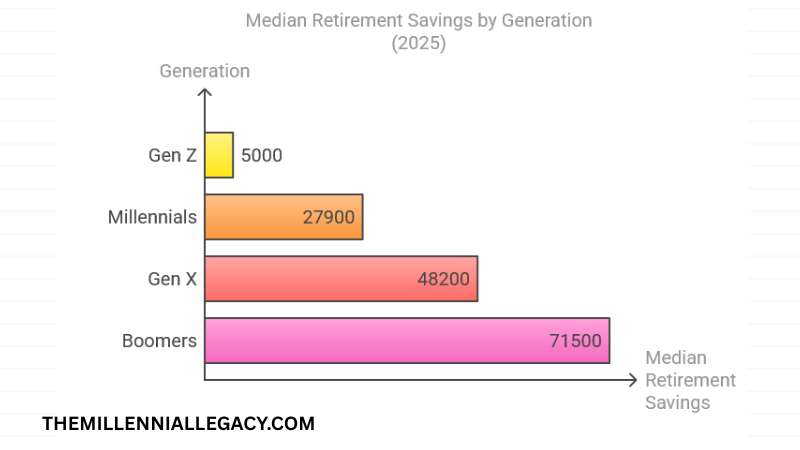

Generational Snapshot: How Each Generation Is Saving

Savings behaviors vary widely across generations—shaped not only by age and life stage but also by economic events, cultural shifts, and financial education. Here’s how Americans are actually saving in 2025, according to available data:

🧪 Gen Z (Ages 13–28): Digital Natives, Cautious Starters

Gen Z is still early in their careers—or in school—but already showing different savings habits. Many use fintech apps, automated investing tools, and round-up features to build small savings passively. Their awareness of financial literacy is high, but their savings levels remain low, largely due to high rent, student debt, and entry-level wages. Still, early participation in Roth IRAs and 401(k)s is more common than it was for Millennials at this age.

According to a 2023 Transamerica report, 67% of Gen Z workers are already saving for retirement.

Millennials faced headwinds from the 2008 financial crisis and rising costs of living, often delaying homeownership, marriage, and saving. Many are now in the “catch-up” phase—balancing childcare, mortgages, and climbing incomes with growing awareness that retirement is no longer far off. While the median retirement savings for Millennials is around $27,900, those numbers are rising.

In 2024, Fidelity reported a 20% increase in Millennial 401(k) contributions compared to the previous year.

⏳ Gen X (Ages 45–60): High Earners, High Pressure

Gen X is often called the “forgotten generation” in financial media—but they are now at peak earning years and facing the most financial pressure. With college expenses for kids, aging parents to care for, and retirement approaching, many Gen Xers report feeling unprepared. The median retirement savings of $48,200 doesn’t match the 6–7x income recommendation for their age bracket, but Gen X contributes the most (percentage-wise) to 401(k) plans today.

A 2023 Bankrate survey found that 49% of Gen Xers fear they won’t be able to retire on time.

🧓 Boomers (Ages 61–79): Entering or Living in Retirement

Boomers are either drawing down their savings or preparing to. While median savings for this group sits at $71,500, it varies drastically depending on income, health, and housing status. Many Boomers rely heavily on Social Security, and some supplement it with pensions, real estate income, or part-time work.

According to Fidelity, Boomers with access to 401(k)s have an average balance over $232,000—but millions are below the median.

As the data shows us, each generation faces unique circumstances, but the pattern is clear:

The earlier the start, the better the outcomes.

Delays in saving compound over time—but so can small wins.

Final Thoughts: You’re Not Behind—You’re Just Getting Started

If you’re asking questions like “how much money should I have saved by 30?” or “what’s the average savings by age 40?”—you’re not failing. You’re planning.

Yes, the averages might feel intimidating. But they’re just data points—not destiny. The most important number in your savings plan isn’t what you have today. It’s what you consistently add from here forward.